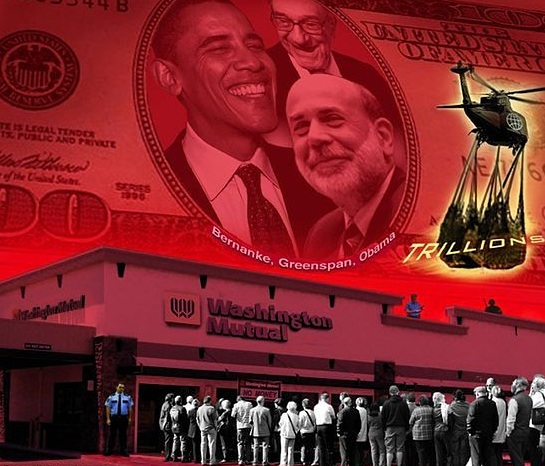

Obama's Depression

Chosen to serve power, not popular interests, Obama wrecked America's economy to save giant Wall Street banks. He's still doing it, despite claiming he's been out in front doing all he can.

By bailing out too-big-to-fail banks and waging multiple imperial wars, he intensified social misery.

As a result, Main Street is mired in protracted Depression. Economist David Rosenberg believes we're in the "third inning" of hard times malaise.

Four occurred in the 19th century. Until now, the 1930s Great Depression was America's last severe downturn, lasting a decade, punctuated by failed bounces.

America's Greatest Depression began in late 2007. Rosenberg calls is a "modern-day" one similar to what Japan experienced for over two decades. It's still ongoing, boding ill for US workers if America replicates Japan's experience.

Depressions occur "once it becomes painfully obvious" that conditions don't improve despite "repeated bouts of policy stimulus."

Most of America's went for banker bailouts, tax cuts for corporate favorites and super-rich elites, as well as quantitative easing money creation for speculation, not economic growth.

In contrast to recessions lasting six to 18 months, depressions last years.

From 2002 - 2007, America's economy was massively manipulated and levered. As a result, financial activities comprised 40% of profits. At the same time, household debt to income and assets "surged to unprecedented levels and the personal savings rate" was negative when the housing bubble peaked. As a result, America experience levered prosperity. Conditions are now reverting to the mean. A long way down remains.

Since fall 2007, GDP, production, real income, and other major economic indicators never recovered to previous cycle highs. In normal times, post-recession tops are achieved and surpassed in a year or less.

Not now. Home sales are 22% lower than in late 2009. Employment growth, in fact, has been stagnant for over a decade. The S&P 500 is no better than in spring 1998. In terms of job creation (what matters most on Main Street) and equity appreciation, America's had a lost decade well into another one.

Recessions usually reflect inventory cycles. Traditional monetary and fiscal stimulus reignites demand.

In contrast, "balance sheet compression and deleveraging" characterize depressions, including debt reduction, asset liquidation, and rising savings as consumers hunker down in hard times.

When excesses produce bubbles, mean reversion is protracted and painful. Structural, not cyclical, problems need fixing. It happened in the 1930s, Japan since 1990, and today in America and Europe, causing global reverberations.

After nearly four years of near-zero interest rates, unprecedented money creation (QE ad infinitum), loan adjustments, and tax cuts, no end is in sight to contracting credit, no job growth, or economic pain, despite tout TV pundits saying otherwise.

Despite fiscal and monetary measures, America's economy "is still saddled with roughly $1 trillion of excess capacity." Moreover, unemployment is shockingly high at nearly 23%.

Again, headline numbers stick to the illusory 9.1% based on most recent data because the formula to compute it was manipulated to lie. Workers without jobs wanting them tell a different tale.

Around 25% idle manufacturing capacity also shows economic trouble, not recovery. As conditions worsen, Rosenberg "shudder(s) at how far operating rates" may fall from current levels.

Two decades of speculative credit expansion created bubble conditions that burst. Despite deleveraging, private sector debt to national income still hovers near a record 137% high, compared to a more normal 80%.

As a result, getting there entails mean reverting from $4 - 6 trillion to bring liability levels to where credit again can expand. It won't happen easily or quickly.

"It will take time and a shared burden by lenders, households and future generations of taxpayers before we hit bottom in this credit contraction."

Expect years before it ends, exacerbated by secular attitude changes toward credit, savings, discretionary spending and homeownership.

Consumers no longer see dwellings as a surefire investment, especially with continuing foreclosures and falling valuations with no end of pain in sight.

Moreover, since late 2007 to mid-2011, an estimated $7 trillion of household net worth was lost. Recouping modest amounts of that will take years, and for older workers nearing retirement it's too late.

"Long and variable lags between changes in household net worth" and consumer spending patterns suggest protracted demand weakness for years. Emphasizing savings and budget priorities will impact most discretionary goods and services negatively.

Ahead, emerging economies will far outdistance America even though global demand overall relied too long on the US consumer for growth. That "well (ran) dry. This time for good," at least for the long term.

Moreover, the combination of rising US savings reducing aggregate demand will be deflationary for years.

It also suggests protracted hard times for beleaguered households, struggling through hardships not helped by counterproductive policies.

They understand it better than Wall Street's best and brightest, getting fat bonuses while working Americans suffer.

___________________________________________________________________________________

Stephen Lendman: I was born in 1934 in Boston, MA. Raised in a modest middle class family, attended public schools, received a BA from Harvard University in 1956 and an MBA from the Wharton School at the University of PA in 1960 following 2 years of obligatory military service in the US Army. Spent the next 6 years as a marketing research analyst for several large US corporations before becoming part of a new small family business in 1967, remaining there until retiring at the end of 1999. Have since devoted my time and efforts to the progressive causes and organizations I support, all involved in working for a more humane and just world for all people everywhere, but especially for the most needy, disadvantaged and oppressed. My efforts since summer 2005 have included writing on a broad range of vital topics ranging from war and peace; social, economic and political equity for all; and justice for all the oppressed peoples of the world like the long-suffering people of Haiti and the Palestinians. Also co-hosting The Global Research News Hour, occasional public talks, and frequent appearances on radio and at times television. Stephen Lendman is a Research Associate of the Centre for Research on Globalization. He lives in Chicago and can be reached at lendmanstephen@sbcglobal.net. Also visit his blog site sjlendman.blogspot.com and listen to The Lendman News Hour on RepublicBroadcasting.org Monday - Friday at 10AM US Central time for cutting-edge discussions with distinguished guests on world and national issues. All programs are archived for easy listening. Stephen's new book "How Wall Street Fleeces America: Privatized Banking, Government Collusion and Class War" can be ordered HERE.

___________________________________________________________________________________

Illustration: David Dees

URL: http://www.a-w-i-p.com/index.php/2011/10/11/obama-s-depression